Private liquor retailers have made big moves in the past year to recapture their dominance with younger consumers, primarily through an increased focus on Ready-To-Drink (RTD) beverages. The pandemic disrupted some shopping behaviours resulting in younger demographics exploring different beverage options, However the recent focus on RTDs appears to have been effective at recapturing shoppers who strayed during the pandemic.

The explosive growth in the RTD space in the past few years has been quite positive for BC’s LRSs. RTDs have grown 30% in BC since 2019, with 1/3 of that volume from consumers under 34. RTDs have a strong bias towards social occasions, usually at someone else’s home or the cabin, with these occasions accounting for twice as much RTD consumption compared to beer or wine.

Naturally, BC’s private retailers have capitalized on this RTD boom. People shopping for RTDs at these retailers are 23% more likely to be shopping for a special occasion or to bring to social gatherings compared to shoppers at government liquor stores. As such, they value convenience, smaller pack sizes, and a wide range of chilled options. In fact, 11% of shoppers purchasing RTDs at private stores specifically cite the product being available chilled as their main reason for purchase. This is 70% greater than government liquor stores.

“Curate your selection based on trends and customer demand.”

When capturing the RTD trend, it’s important to curate your selection based on trends and customer demand. A full 15% of RTD shoppers at LRSs say they could not find the product they were looking for, compared to just 1% in GLSs. Fortunately, this does not appear to deter purchasing altogether as shoppers will usually find an acceptable alternative on the shelf. This does highlight the challenge of maintaining a diverse and current brand selection, though. Especially in a category that moves quickly and where shelf or fridge space are at a premium. Shoppers may sometimes be willing to switch based on available inventory, but there’s only so many times retailers can expect them to settle for second choice.

The convenience and popularity of RTDs has helped BC’s private retailers maintain pricing power. Only 21% of their total sales and 8% of their RTD sales appear to be motivated by price discounts. This compares to 26% and 20% respectively for government liquor stores.

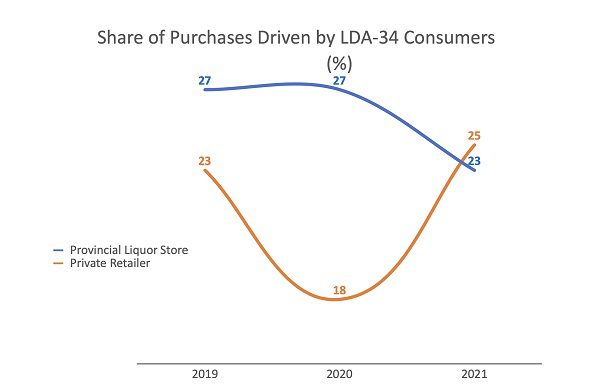

LRSs have found a winning formula, by emphasizing convenience and a product selection that demands said convenience, they’ve been able to win a greater share of younger shoppers while maintaining pricing power. In contrast, it appears that GLSs may be failing to build a relationship with younger demographics for the long term.

Ken Field is a Director at Ipsos North America where he leads their alcohol consumption tracking research supporting some of North America’s largest brands.